Reverse Mortgage Scam

How fraudulent schemes exploit the reverse mortgage process to strip older homeowners of their home equity - and sometimes their homes entirely

Reverse mortgage scams target homeowners 62 and older who are considering accessing their home equity. The consequences can include losing the equity built over a lifetime - or losing the home itself.

In This Guide

- Overview of the Scam

- How the Scam Works

- Common Variations

- Example Scam Messages or Pop-Ups

- Warning Signs

- Who Scammers Often Target

- What the Scammer Is Trying to Achieve

- What To Do If You Encounter This Scam

- If You Already Paid or Shared Information

- How To Prevent Reverse Mortgage Scams

- Final Safety Advice

Overview of the Scam

Reverse mortgage scams exploit the legitimate Home Equity Conversion Mortgage (HECM) program - a federally insured loan available to homeowners 62 and older that allows them to access their home equity without monthly payments. Fraudsters use the real appeal of this program as a vehicle for schemes that divert the loan proceeds, forge documents, or manipulate homeowners into transactions that strip their equity and, in the worst cases, result in foreclosure.

For many older adults, their home is their most significant financial asset and represents decades of work and savings. Reverse mortgage fraud can eliminate that equity in a single transaction. The complexity of reverse mortgage products and the often high-pressure or confusing sales environments in which they are presented make these scams particularly dangerous.

Legitimate reverse mortgages are a regulated financial product that, when used appropriately, can genuinely help older homeowners. The problem lies in fraudulent versions of these transactions and in third parties who exploit the product to serve their own financial interests at the expense of the homeowner.

How the Scam Works

Reverse mortgage scams take several forms, but the most common involve third parties who recruit homeowners for transactions that primarily benefit the recruiter.

- A homeowner is contacted by someone offering a financial solution to a problem - help with home repairs, an investment opportunity, a way to generate retirement income. The solution involves taking out a reverse mortgage on their home.

- The third party - a contractor, investor, or financial promoter - facilitates the reverse mortgage application, often using their own preferred lender and title company. The homeowner may not fully understand the transaction they are entering or its long-term consequences.

- The reverse mortgage proceeds - which can be substantial, representing a significant portion of the home's value - are disbursed. The third party takes their cut of the proceeds through inflated fees, fake services, or direct diversion. The homeowner receives far less than they expected, or nothing at all.

- The homeowner is now legally obligated to maintain the home, pay property taxes and insurance, and live in the home as their primary residence - or face foreclosure. If the third party used the funds without their knowledge, the homeowner may be in default with no resources to remedy it.

- In fraudulent flipping schemes, the property may change hands multiple times with inflated appraisals, leaving the homeowner's equity extracted and the lender holding a loan that exceeds the home's actual value.

Common Variations

Reverse mortgage fraud takes several specific forms, each designed to extract equity from the homeowner through different mechanisms.

- Home repair scheme: A contractor offers significant home repairs - a new roof, foundation work, accessibility modifications - and suggests a reverse mortgage to fund them. The contractor facilitates the loan, performs minimal or shoddy work, and takes most of the proceeds. The homeowner is left with a depleted equity and substandard repairs.

- Investment scheme: A financial promoter suggests taking out a reverse mortgage and investing the proceeds in a high-return investment they manage. The investment is fraudulent and the proceeds are stolen. The homeowner has encumbered their home equity for nothing.

- Document forgery: A scammer forges the homeowner's signature on reverse mortgage documents without their knowledge, takes the loan proceeds, and disappears. The homeowner discovers the loan only when notified by the lender or when foreclosure proceedings begin.

- Caretaker or family member fraud: A trusted caretaker, family member, or advisor manipulates or coerces an older homeowner into taking out a reverse mortgage and directing the proceeds to them under false pretenses.

- Straw buyer scheme: A more complex fraud involving third parties who use the homeowner's property in a series of transactions with inflated appraisals, extracting equity through the process while leaving the homeowner with legal and financial liability.

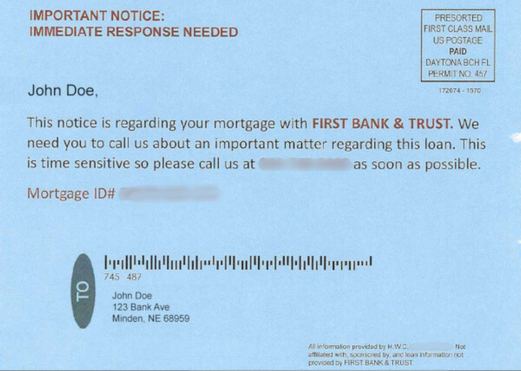

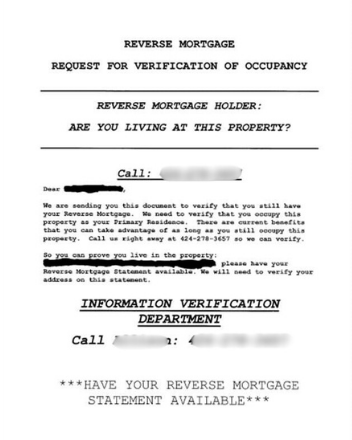

Example Scam Messages or Pop-Ups

The example below shows the type of communication and approach used to introduce a reverse mortgage scam. These pitches often emphasize the benefits of accessing home equity while minimizing or obscuring the risks and conditions involved.

The solicitation emphasizes the homeowner's equity as a resource that is going unused - framing the reverse mortgage as simply accessing what is already theirs. The connection to a specific contractor or investment is introduced as a convenience rather than a conflict of interest. A legitimate reverse mortgage transaction does not require or encourage the homeowner to direct proceeds to a third party - the decision about how funds are used should be entirely the homeowner's own.

Common language in reverse mortgage scam pitches includes: "You have hundreds of thousands of dollars sitting in your home doing nothing - a reverse mortgage lets you access it tax-free with no monthly payments," "We handle all the paperwork, the repairs get done, and the reverse mortgage pays for everything - you don't pay a cent out of pocket," and "This investment program is specifically designed for reverse mortgage recipients - your money works harder for you than equity sitting in a house."

Warning Signs

These signals indicate that a reverse mortgage transaction or solicitation may involve fraud or exploitation.

- A contractor, investor, or third party is steering you toward a specific reverse mortgage lender or suggesting you take out a reverse mortgage to fund their services or investments.

- Someone is discouraging you from attending HUD-required counseling, trying to rush through the process before counseling can take place, or suggesting the counseling is just a formality.

- You are being asked to sign documents you have not read or do not understand, or are being pressured to close quickly before you have had time to review everything carefully.

- The proceeds from the reverse mortgage are being directed to a third party's account rather than to you directly, or you are being asked to immediately transfer proceeds to pay for services or investments.

- The person facilitating the transaction has a financial interest in the outcome - earning a fee or commission - beyond the standard compensation of a licensed lender or broker.

- No independent attorney, advisor, or family member has reviewed the transaction with you. Any legitimate significant financial transaction benefits from independent review.

- You feel pressured, confused, or uncertain about what you are agreeing to - but the other party is discouraging you from asking more questions or taking more time.

Who Scammers Often Target

Reverse mortgage scams specifically target homeowners aged 62 and older who have significant home equity and who may be experiencing financial stress - needing income in retirement, facing large repair bills, or looking for ways to make their savings go further. The combination of significant assets and financial pressure is the profile these scams are designed for.

Homeowners who are in poor health, recently widowed, or in early cognitive decline are more vulnerable because they may be less able to critically evaluate complex financial transactions and more likely to trust whoever is facilitating the process on their behalf.

People in neighborhoods with older housing stock - where maintenance costs are real and significant - are frequently targeted by contractor-based reverse mortgage schemes that appear to solve a genuine problem.

What the Scammer Is Trying to Achieve

The goal is the equity in the homeowner's property - typically the largest financial asset they own. Reverse mortgage fraud can extract tens or hundreds of thousands of dollars from a single transaction. Because the homeowner's home is the collateral, the consequences of fraud extend beyond financial loss to the potential loss of the home itself through foreclosure.

In investment-based schemes, the goal is the loan proceeds themselves - taken through a fraudulent investment product and never returned. In contractor schemes, the goal is inflated fees for services that are never fully delivered. In all cases, the homeowner's equity disappears while the obligation attached to it remains.

What To Do If You Encounter This Scam

If you are considering a reverse mortgage and have concerns about the transaction or the people involved, here is how to protect yourself.

- Attend HUD-approved counseling independently. This is required for legitimate HECM loans and is one of your most important protections. The counselor is on your side and not paid by the lender. Find a HUD-approved counselor at hud.gov.

- Bring a trusted family member, friend, or independent attorney to review any documents before signing. You are entitled to take as much time as you need before closing.

- Be very cautious if the reverse mortgage was suggested by someone who has a financial stake in the outcome - a contractor who will be paid from proceeds, an investor offering to use the funds, or anyone whose compensation depends on you taking out the loan.

- Contact HUD's Office of Inspector General or the Consumer Financial Protection Bureau at consumerfinance.gov if you believe you have encountered fraud in connection with a reverse mortgage offer.

How To Prevent Reverse Mortgage Scams

These steps protect you if you are considering a legitimate reverse mortgage or have been approached about one.

- Only work with HUD-approved HECM lenders and complete the required independent counseling before signing anything. The counseling is free and specifically designed to ensure you understand what you are agreeing to.

- Never take out a reverse mortgage at the suggestion of a contractor, investor, or anyone else who will benefit financially from the transaction. The decision to take a reverse mortgage should be yours alone, made with independent advice.

- Have an independent attorney review all documents before closing. This is especially important for a transaction involving your home.

- Take your time. There is no legitimate reverse mortgage that must close today or this week. Any pressure to rush is a warning sign.

- Talk to family members or a trusted independent financial advisor before proceeding. An outside perspective on a major financial decision involving your home is always valuable.

Final Safety Advice

Reverse mortgage fraud can have consequences that are difficult or impossible to reverse - home equity built over decades can be gone in a single transaction, and in the worst cases the home itself can be lost. The stakes are as high as they get in personal finance, which makes taking the time to protect yourself not just worthwhile but essential.

The protections available are real and meaningful: the required HUD counseling, the legal rescission period, and the availability of independent legal and financial advice. These safeguards exist specifically because legitimate reverse mortgages are complex and consequential transactions that benefit from independent oversight. Using them fully is not a sign of distrust toward a lender - it is simply responsible financial decision-making.

If you believe fraud has already occurred, act quickly. The rescission period is time-limited, and the sooner legal and regulatory action is initiated, the more options remain available. Elder law attorneys and HUD counselors are experienced with these situations and can advise you on the specific options in your circumstances.