Debt Collection Scam

How fake debt collectors use threats of arrest, lawsuits, and wage garnishment to pressure you into paying debts that may not even exist

Fake debt collectors use fear and urgency to collect money for debts that are either fabricated, already paid, or legally uncollectable. Knowing your rights under federal law is one of the strongest protections you have.

In This Guide

- Overview of the Scam

- How the Scam Works

- Common Variations

- Example Scam Messages or Pop-Ups

- Warning Signs

- Who Scammers Often Target

- What the Scammer Is Trying to Achieve

- What To Do If You Encounter This Scam

- If You Already Paid or Shared Information

- How To Prevent Debt Collection Scams

- Final Safety Advice

Overview of the Scam

A debt collection scam occurs when someone calls or contacts you claiming you owe money - for a payday loan, a credit card, a medical bill, or another debt - and threatens serious consequences if you do not pay immediately. The debt they describe may be entirely fabricated, may relate to a debt you already paid or that is past the statute of limitations, or may be a real but illegitimately purchased debt being collected in an illegal way.

What distinguishes scam collectors from legitimate ones is their behavior. They use illegal tactics - threats of immediate arrest, calls to your workplace or family members to harass you, refusal to provide information about the debt in writing, and demands for unusual payment methods like gift cards or wire transfers. Real debt collectors operate under the Fair Debt Collection Practices Act, which gives you specific rights including the right to request written verification of any debt before paying.

These scams are particularly effective because many people have at some point had a financial obligation they were not fully current on, which makes the claim feel plausible enough to create fear. Understanding your rights and how to verify a debt protects you from paying money you may not owe.

How the Scam Works

Fake debt collection scams follow a consistent pattern built on pressure, urgency, and the threat of legal consequences.

- You receive a call from someone claiming to be a debt collector, a legal process server, a sheriff's deputy, or an attorney. They say you owe a specific amount on a debt - often a payday loan or credit card - and that legal action has already been filed or is imminent.

- The caller provides just enough specific-sounding detail to seem credible - a case number, a creditor name, or the last four digits of a financial account - without providing the full documentation a legitimate collector is required to give you.

- They threaten serious consequences unless you pay immediately: arrest, a lawsuit, wage garnishment, or a visit from law enforcement. These threats are designed to make you feel that any delay will make the situation dramatically worse.

- You are told to pay right away using an unusual method - a wire transfer, a prepaid debit card, a gift card, or a money order sent to a specific address. The unusual payment method is both a red flag and the reason recovery is impossible if you pay.

- If you pay, the scammer may call back with additional "debt" claims knowing you have paid once. If you do not pay, they may continue calling with escalating threats or simply move on to other targets.

Common Variations

Debt collection scams take several forms depending on the type of debt claimed and the approach used.

- Payday loan scam: The most common version. Callers claim you took out a payday loan that was never repaid and that legal action is being filed. Many victims did take out payday loans at some point, which makes the claim feel plausible even when the specific debt is fabricated.

- Zombie debt collection: A real debt is purchased - often for pennies - and collected even though it is past the statute of limitations for legal action. The collector cannot legally sue you over it, but they call and threaten lawsuit anyway. Paying may actually restart the statute of limitations clock.

- Legal process server impersonation: The caller claims to be serving legal papers or delivering a summons and says you must call a callback number immediately to arrange a settlement before being served in person.

- "Arrest warrant" version: The caller claims a warrant has been issued for your arrest related to the unpaid debt and that only immediate payment can stop the arrest from being carried out. Debt is a civil matter in the US - you cannot be arrested for not paying a private debt.

- Medical debt version: Using information obtained from data breaches or purchased lists, callers claim you have an unpaid medical balance and threaten to refer it to attorneys or report it to credit bureaus unless paid immediately.

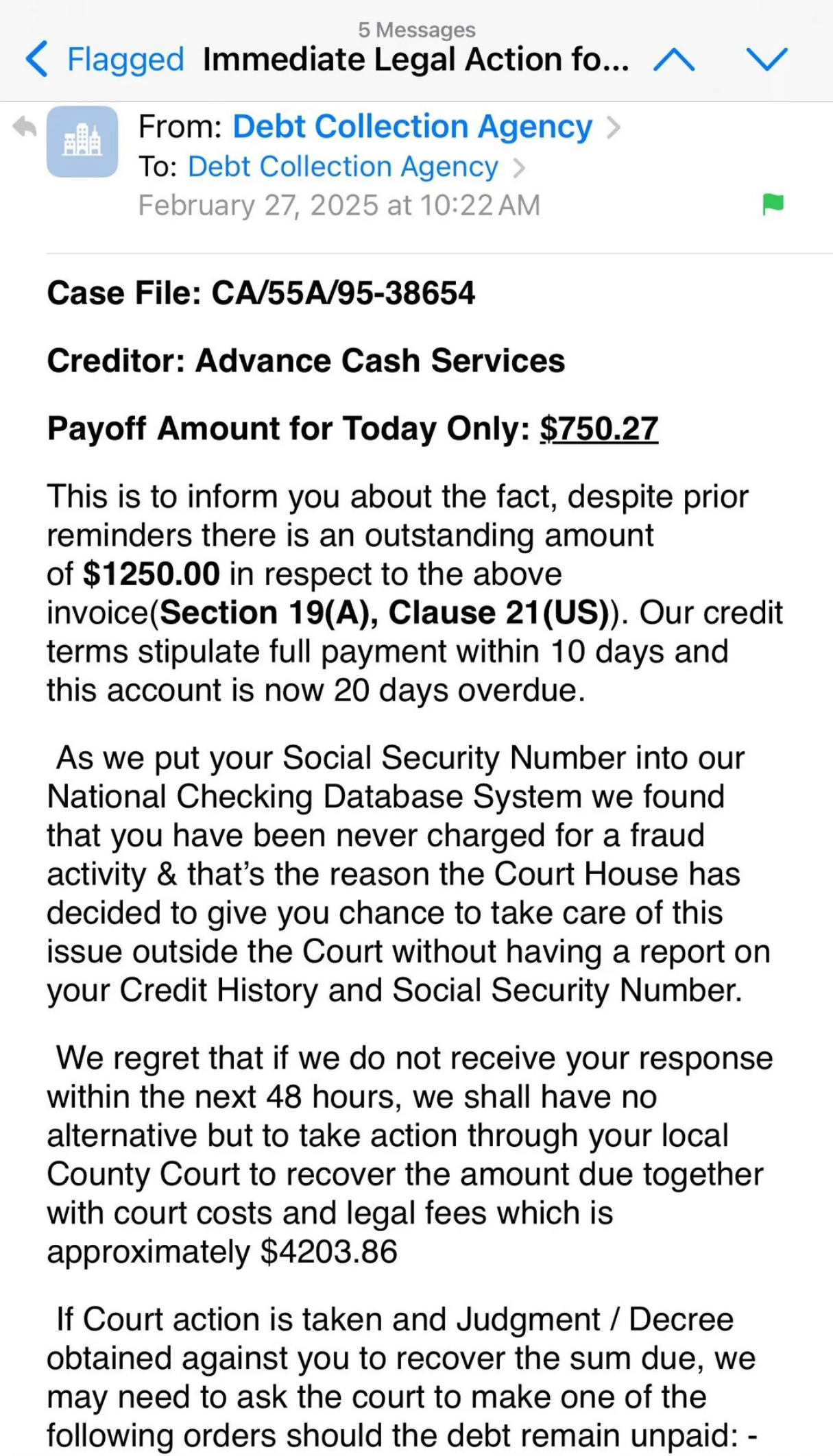

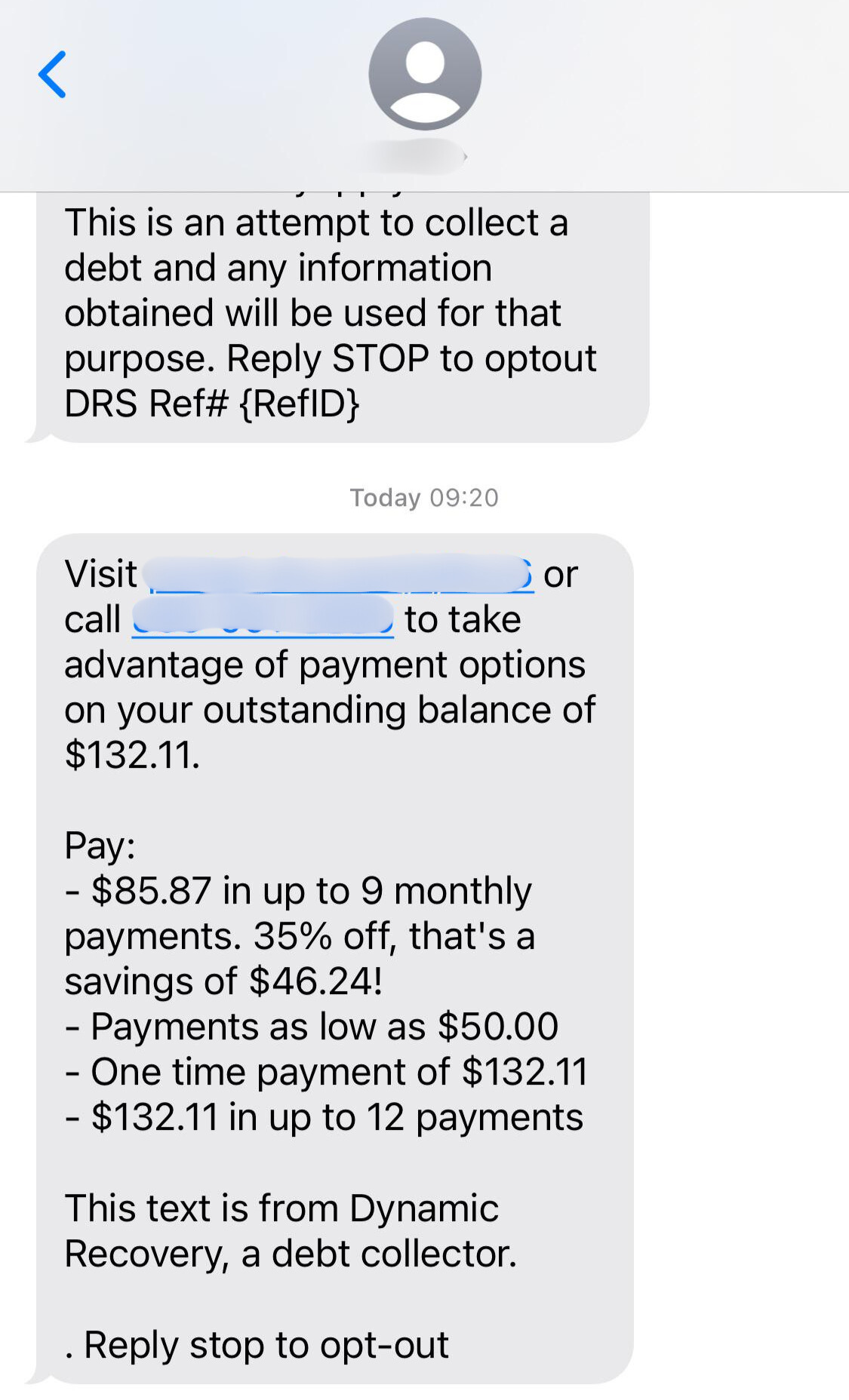

Example Scam Messages or Pop-Ups

The example below shows the type of voicemail or follow-up message left by fake debt collectors. The tone is deliberately legal-sounding and threatening.

Notice the use of legal-sounding terminology, a case number, and the threat of immediate consequences. Real debt collectors are prohibited from threatening actions they cannot or will not take - including arrest for a civil debt. The demand for immediate payment via an untraceable method and the refusal to provide written documentation of the debt are the clearest indicators that this contact is fraudulent.

Typical language includes: "This is a final notification before legal proceedings are initiated against you for an outstanding debt of $847. You have until 5pm today to contact our office at [number] to arrange payment and avoid a civil judgment," and "A warrant has been issued for your arrest in connection with a delinquent account. Call immediately to discuss a settlement arrangement before law enforcement is dispatched to your address."

Warning Signs

These behaviors consistently indicate a debt collection call is fraudulent or illegal rather than legitimate.

- The caller threatens immediate arrest or criminal charges for the unpaid debt. This is not legally possible for private debts in the US and is a definitive red flag.

- The caller refuses to provide the name of the original creditor, the amount of the debt, or written verification of the debt when you request it. This refusal violates federal law for legitimate collectors.

- Payment is demanded immediately and only through a method that cannot be traced or reversed - gift cards, wire transfer, prepaid debit cards, or cryptocurrency.

- The caller is aggressive, threatening, or uses obscene language. The Fair Debt Collection Practices Act prohibits these behaviors in legitimate collection calls.

- The caller threatens to contact your employer, your family, or your neighbors about the debt. Legitimate collectors are heavily restricted in who they can contact and why.

- The debt they describe is one you have never heard of, already paid, or that you believe is far past its collection period.

- The caller refuses to send information by mail or email and insists the debt must be paid by phone right now to avoid consequences.

- A case number or legal reference is given but cannot be verified through any court record system or legal search.

Who Scammers Often Target

Fake debt collectors target people broadly, using purchased data lists that may include names, addresses, and in some cases partial financial information obtained from data breaches. People who have had any financial difficulty - a lapsed account, a payday loan, medical debt - are more likely to believe a claim about an outstanding balance.

People who are unfamiliar with their rights under the Fair Debt Collection Practices Act are more vulnerable because they do not know they can legally demand written verification before paying anything. This knowledge gap is significant - many people feel they have no choice but to engage with or comply with whoever calls claiming to be a debt collector.

Older adults are frequently targeted because they are more likely to respond to authority-sounding calls and may be more worried about any threat involving legal consequences or credit reporting.

What the Scammer Is Trying to Achieve

The goal is payment - for a debt that may not exist at all, may already be resolved, or may not be legally collectible. Because the caller uses legal-sounding threats, victims often pay out of fear rather than because they genuinely believe they owe the money.

In some cases, the scammer is also harvesting personal information - Social Security numbers, bank account details, date of birth - under the guise of verifying the account before processing a payment. This information is used for identity theft independent of any payment made.

What To Do If You Encounter This Scam

If you receive a threatening debt collection call, you have rights and options that put you in a strong position.

- Ask for the collector's name, company name, address, and phone number, and the name of the original creditor. Legitimate collectors are required by law to provide this information. Write it down.

- Request written verification of the debt. Say: "I am requesting debt verification in writing as I am entitled to under the Fair Debt Collection Practices Act." A legitimate collector must cease collection activity until they provide this. A scammer will refuse or escalate their threats.

- Do not pay anything over the phone, especially via gift card, wire transfer, or prepaid card. Paying through these methods with an unknown collector confirms that payment works and may result in further demands.

- Check your credit reports at AnnualCreditReport.com to see whether the debt claimed appears there from any recognizable creditor. If no such debt exists in your credit history, the claim is almost certainly fraudulent.

- Report the call to the FTC at ReportFraud.ftc.gov and to the Consumer Financial Protection Bureau at ConsumerFinance.gov. If you received threats involving arrest, you can also report it to your state attorney general's office.

How To Prevent Debt Collection Scams

Understanding your rights and knowing what legitimate debt collection looks like are your most powerful protections.

- Know that you have the right to written verification of any debt before paying. This is guaranteed under federal law. Exercise this right whenever you receive an unexpected collection call.

- Never pay a debt via gift card, wire transfer, or prepaid debit card. Legitimate debt collectors accept checks, electronic bank transfers, and credit card payments - all traceable and reversible through dispute processes.

- Check your credit reports regularly. Knowing what debts legitimately appear in your history makes it easier to recognize when a collection call is about something that does not exist.

- If a debt collector calls, verify the company independently before engaging further. Look up their name and check for complaints with the Better Business Bureau and your state attorney general's office.

- Know that you cannot be arrested for a private, civil debt in the US. Any call claiming otherwise is illegal and is almost certainly a scam. This knowledge alone removes the most powerful tool these callers have.

Final Safety Advice

Debt collection scams are effective because they use legal-sounding language, specific-seeming details, and the threat of serious consequences to create fear. That fear is designed to override the impulse to stop and ask questions - including the question of whether the debt is real at all.

The knowledge that protects you most is this: you have the right to request written verification of any debt, and no legitimate collector can continue pursuing you until they provide it. Exercising that right costs you nothing and immediately separates real collectors from scammers. A real collector will send the verification. A scammer will either hang up or escalate threats - and that response tells you everything.

If you have already sent money or provided information, act quickly to protect your accounts and report the fraud. These scams are well-documented and actively investigated - your report contributes to efforts to stop them. And please do not carry the shame of having been targeted. These operations are designed by people whose full-time work is to make the threat feel real. Your response was entirely understandable.