Fake Check Scam

How fraudulent checks trick victims into sending real money before the check bounces days later

Fake checks are often indistinguishable from real ones - they may even clear initially when deposited. The trap closes days later when the check bounces, leaving the victim responsible for any money their bank advanced.

In This Guide

- Overview of the Scam

- How the Scam Works

- Common Variations

- Example Scam Messages or Pop-Ups

- Warning Signs

- Who Scammers Often Target

- What the Scammer Is Trying to Achieve

- What To Do If You Encounter This Scam

- If You Already Paid or Shared Information

- How To Prevent Fake Check Scams

- Final Safety Advice

Overview of the Scam

A fake check scam works by sending you a fraudulent check - one that may look completely legitimate - and then asking you to deposit it and wire or send back a portion of the funds. The check clears initially because banks make funds available quickly, but it bounces days later when it is returned as fraudulent. By then, the money you sent is gone, and you are left responsible for the full amount of the original check.

The core deception exploits a banking rule many people do not know: when you deposit a check, your bank makes the funds available within one to a few business days, but the process of fully verifying whether the check is legitimate can take up to several weeks. If the check is eventually returned as fraudulent, your bank will withdraw the full amount from your account - even if you have already spent or sent some of it.

Fake check scams appear in many different contexts - overpayment for items you are selling, lottery winnings, job offers, and more - but the structure is always the same: you receive a check, deposit it, send back a portion, and the original check later bounces.

How the Scam Works

The scam exploits the timing gap between when funds appear available in your account and when a check is fully verified as legitimate.

- You receive a check in the mail or are told one is coming. The context varies - it might be framed as payment for a job, a prize, a purchase someone is making from you, or an overpayment that needs to be returned.

- The check looks legitimate. It may be printed on real check stock, carry the name of an actual business or bank, include authentic-looking security features, and be for a specific and believable amount.

- You are asked to deposit the check and then send back a portion - usually described as a fee, an overage, shipping costs, taxes, or a share of the proceeds. You are told to wire the money, buy gift cards, or send via a payment app before the check has been fully processed.

- You deposit the check and see the funds appear in your account. This feels like confirmation that the check is legitimate. You send the requested amount back as instructed.

- Several days to weeks later, the bank discovers the check is fraudulent and reverses the deposit. Your account is debited for the full amount of the original check. The money you sent earlier is gone with no way to recover it.

Common Variations

Fake check scams appear in several different scenarios, each designed to make the check feel like a natural and expected part of a transaction.

- Overpayment scam: You are selling something - a car, furniture, or an item listed online - and the buyer sends a check for more than the asking price, asking you to deposit it and wire back the difference. The check is fake, the overpayment is a lie, and the "difference" you wire is a real loss.

- Mystery shopper scam: You are hired as a mystery shopper and receive a check to fund your assignments. You are asked to wire part of it to evaluate a money transfer service. The check bounces and you are responsible for the amount you wired.

- Work-from-home job scam: A new remote job requires you to receive checks and forward funds as part of your role. You are essentially being used as a money mule - processing fraudulent checks on behalf of scammers.

- Prize or lottery version: A check arrives with a sweepstakes notification, representing a portion of your winnings. You are asked to deposit it and wire back the taxes or processing fee. The check is fake.

- Rental scam: A prospective tenant for a property you are renting sends a check for more than the deposit and asks you to wire back the difference before they arrive. The check bounces after you send the money.

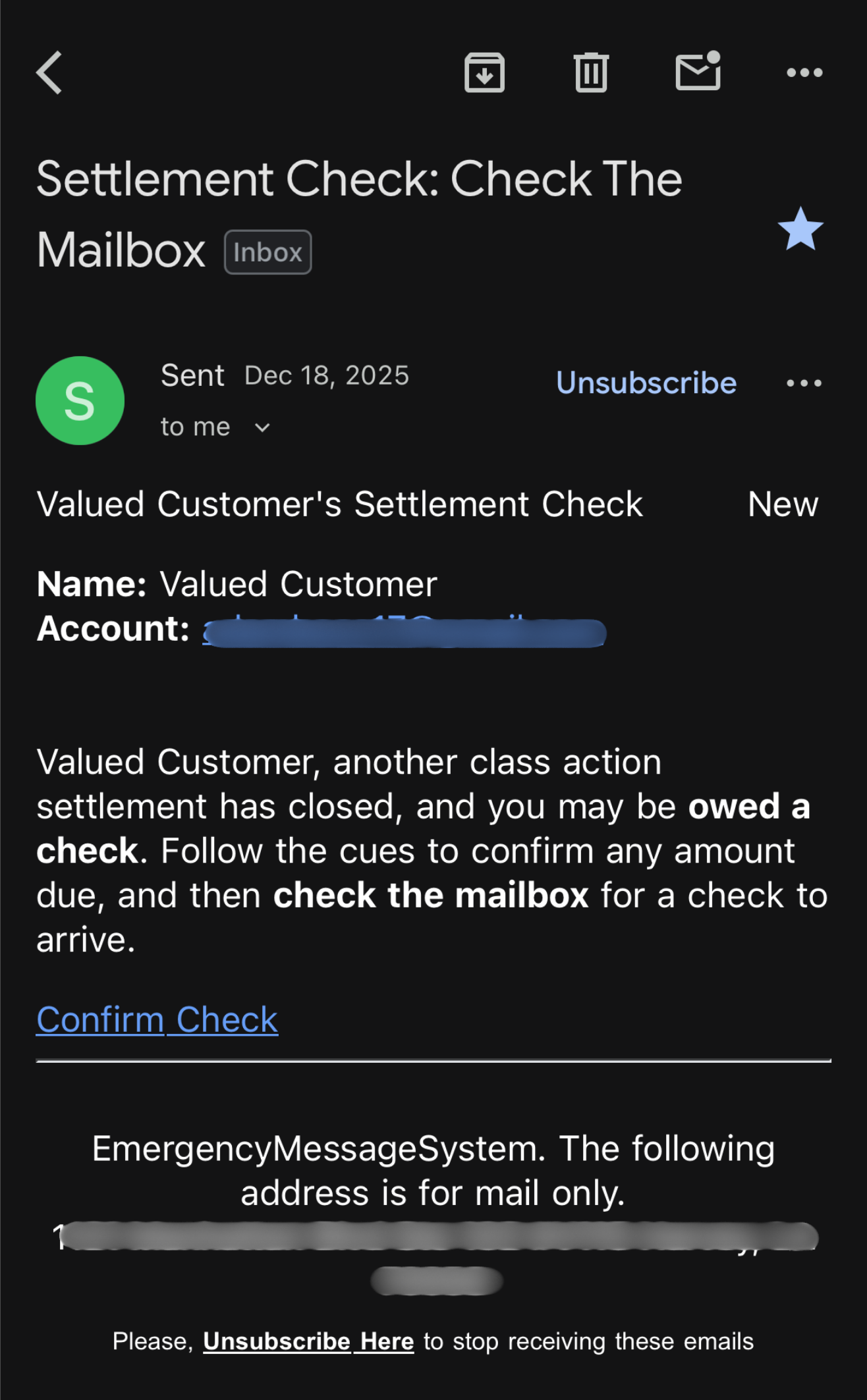

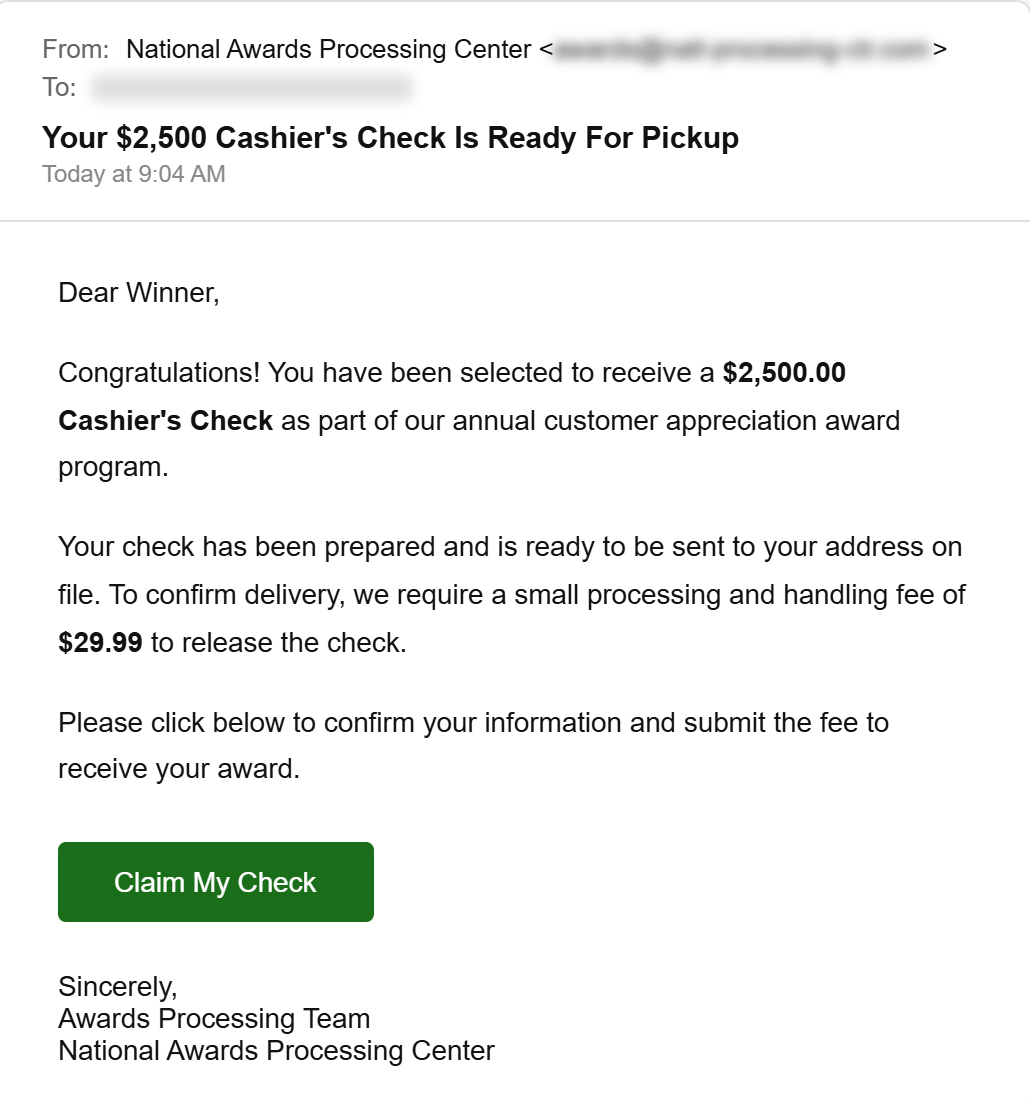

Example Scam Messages or Pop-Ups

The example below shows how fake check scam instructions typically look when they arrive alongside a fraudulent check. The communication is designed to make the request seem routine and logical.

The letter creates an ordinary-sounding reason for the overpayment and makes the request to wire back funds seem like a simple administrative step. The check itself will look real and may even carry the name of a legitimate bank. The only way to catch this before it is too late is to recognize the pattern - any situation where you are asked to deposit a check and send back money is a scam.

Sample language from fake check scam communications includes: "I am sending you a check for $3,500 - please deposit it and wire $1,800 back to my assistant to cover shipping and handling," "Please cash the enclosed cashier's check and forward $900 via Zelle for taxes before we can process your mystery shopping assignments," and "The check is for the full amount - please send us back the difference of $2,200 via gift cards once it has cleared."

Warning Signs

These signals indicate a check-based transaction is fraudulent and should not be acted on.

- You are asked to deposit a check and send back any portion of it - via wire transfer, gift cards, a payment app, or any other method. This structure is the defining characteristic of fake check fraud.

- A buyer, employer, or contest sends you a check for more than the agreed amount and asks you to return the difference.

- A new job or work-from-home arrangement involves receiving checks and forwarding money to someone else. This is a money mule setup, often involving fraudulent checks.

- You are told to act quickly and send the money back before the check has fully cleared - creating time pressure that discourages waiting for full verification.

- The check arrives from someone you have never met in person, often in connection with an online transaction, a job posting, or a prize notification.

- The check is for a very specific, unusual amount - not a round number - which is sometimes used to make it appear more legitimate and business-like.

- The reason for the overpayment or check is vague, changes, or does not hold up to basic scrutiny when you ask follow-up questions.

Who Scammers Often Target

Fake check scams target people who are engaged in financial transactions where receiving a check from someone they do not know well is plausible. People selling items on Craigslist, Facebook Marketplace, or similar platforms are frequent targets because the check can be framed as payment from a remote buyer.

People looking for work - especially remote work or flexible income - are targeted through job postings and mystery shopper offers. The promise of easy income combined with the apparently real check makes the scenario feel credible.

Anyone who does not know the specific rule about check clearance timing is vulnerable. Many people reasonably assume that if a check clears, it is legitimate. The gap between fund availability and full verification is not commonly understood, which is exactly what these scams exploit.

What the Scammer Is Trying to Achieve

The goal is to receive real money from the victim - wire transfers, gift card codes, or payment app transactions - before the fraudulent check is detected and reversed. Because the scammer never actually provided any real funds, every dollar the victim sends back is pure profit for the scammer and a direct loss for the victim.

The timing is deliberate. Scammers push for fast wire-backs because the sooner the money is sent, the less likely the victim will have time to realize something is wrong before it is too late to reverse the transaction.

What To Do If You Encounter This Scam

If you receive a check along with a request to send back money, here is what to do.

- Do not deposit the check. If you have already deposited it, contact your bank immediately and explain that you believe the check may be fraudulent. Ask them to place a hold on the funds and not to allow any withdrawals based on that deposit.

- Do not send any money back. Even if the check appears to have cleared, the clearing is provisional. The check can still bounce days or weeks later.

- If you received the check in connection with a job offer, sale, or contest, do not continue with that transaction. The entire arrangement is fraudulent.

- Report the situation to the FTC at ReportFraud.ftc.gov and to your state attorney general's office. If the check arrived by mail, you can also report it to the US Postal Inspection Service.

- If the check was connected to an online marketplace like Craigslist or Facebook Marketplace, report the buyer or seller account to the platform.

How To Prevent Fake Check Scams

These habits protect you from fake check fraud in any context.

- Never deposit a check and send back any portion of it, for any reason. This pattern - receive a check, send back money - is the signature of this scam and is never part of a legitimate transaction.

- When selling online, accept payment only through methods that are fully settled and verified before you ship or transfer anything. Cash in person, or confirmed electronic payments directly to your account, are safer than checks from unknown buyers.

- If a job offer involves receiving and forwarding checks or money, it is a scam. Legitimate employers do not need employees to handle payments this way.

- Wait the full verification period before spending deposited funds if you have any reason to question a check's legitimacy. Ask your bank specifically how long it takes for a check to be fully cleared - not just initially available.

- Be skeptical of any check from someone you have not met in person, particularly when the transaction originated online or through a mailing.

- If something feels slightly off about a transaction involving a check - the buyer is unusually eager, the amount is odd, the story has changed - trust that instinct and pause before depositing anything.

Final Safety Advice

Fake check scams are effective because they exploit a banking process that most people are not familiar with - the difference between when funds become available and when a check is fully verified. When a check appears to clear, it is natural to assume the money is real. The window between those two events is where the scam lives.

The single most protective rule is this: if you receive a check and are asked to send any money back - for any reason and in any amount - do not do it. There is no legitimate scenario in which this is a normal part of a transaction. The check is always fake, and the money you send will always be real.

If you have already been affected, contact your bank immediately and report the situation to the FTC. Being proactive about the bounced check gives you the best chance of managing the financial impact. And sharing what happened with others helps protect your community from the same fraud.