Bank Impersonation Scam

How fraudsters pose as your bank's fraud department to gain access to your accounts and steal your money

Scammers pose as bank fraud departments, spoofing real bank phone numbers and using urgent language to convince you to hand over account access or transfer your own money to them.

In This Guide

- Overview of the Scam

- How the Scam Works

- Common Variations

- Example Scam Messages or Pop-Ups

- Warning Signs

- Who Scammers Often Target

- What the Scammer Is Trying to Achieve

- What To Do If You Encounter This Scam

- If You Already Paid or Shared Information

- How To Prevent Bank Impersonation Scams

- Final Safety Advice

Overview of the Scam

A bank impersonation scam is a type of fraud where someone pretends to be a representative from your bank - most often from the fraud or security department - and contacts you with an urgent warning about suspicious activity on your account. The goal is to convince you to share your account credentials, verify personal information, or transfer your own money somewhere the scammer can access it.

These scams are particularly effective because they mimic something your bank actually does. Banks do contact customers about fraud. They do ask you to verify transactions. They do alert you when something looks unusual. Scammers have studied this process carefully and designed their approach to follow the same script, making it genuinely difficult to tell the difference in the moment.

Bank impersonation scams consistently rank among the highest-loss fraud categories. Because they target your actual bank account directly and often involve convincing you to initiate transfers yourself, the financial damage can be severe and recovery is frequently difficult.

How the Scam Works

The scam typically begins with an unexpected call, text, or email that appears to come from your bank. The sequence is designed to feel like a legitimate fraud prevention process.

- You receive a call, text, or email appearing to come from your bank. The caller ID may display your bank's actual phone number, which can be faked using widely available technology. A text message may even appear in the same thread as previous legitimate bank messages.

- The message tells you that suspicious or unauthorized activity has been detected on your account. The scammer may reference a specific dollar amount, a merchant name, or a location to make the alert feel grounded and real.

- You are told that to protect your account, you need to act immediately. The urgency is deliberate - every minute of hesitation is framed as money at risk. This pressure is designed to prevent you from pausing to independently verify the contact.

- The fake representative walks you through a process to secure your account. This typically involves asking you to verify your identity by providing your account number, PIN, online banking password, or a one-time passcode that was sent to your phone.

- In more sophisticated versions, the scammer tells you that your account has been compromised by a bank employee or an internal breach, and that to protect your funds you need to move them to a temporary safe account that they control. This is called a "safe account" scam.

- Once they have your credentials or you have transferred funds, the scammer either accesses your account directly or disappears with the transferred money. In either case, recovering the funds is extremely difficult.

Your real bank will never ask you for your full password, PIN, or one-time passcodes over the phone. And it will never instruct you to move money to a different account to keep it safe.

Common Variations

Bank impersonation scams take several forms, each designed to exploit a different aspect of how banks actually communicate with customers.

- Fraud alert calls: A caller claiming to be from your bank's fraud department says a suspicious charge has been flagged and asks you to confirm whether you authorized it. The conversation then moves toward verifying your identity in a way that hands over your credentials.

- Safe account transfers: The caller claims your account has been compromised - sometimes blaming an inside employee - and says your money needs to be moved to a secure holding account immediately. The holding account belongs to the scammer.

- Text message alerts: A text arrives appearing to come from your bank about a suspicious transaction, with a link to verify your account or a number to call. These texts may appear in the same conversation thread as real bank messages.

- Online banking phishing: An email with your bank's logo and formatting directs you to a fake login page where your username, password, and security answers are captured.

- Zelle and wire transfer scams: After gaining your trust, the caller walks you through sending money to yourself through Zelle or a wire transfer - which actually goes to the scammer's account.

- Debit card suspension warnings: A message says your debit card has been suspended due to suspected fraud and you need to verify your card number, expiration date, and PIN to restore it.

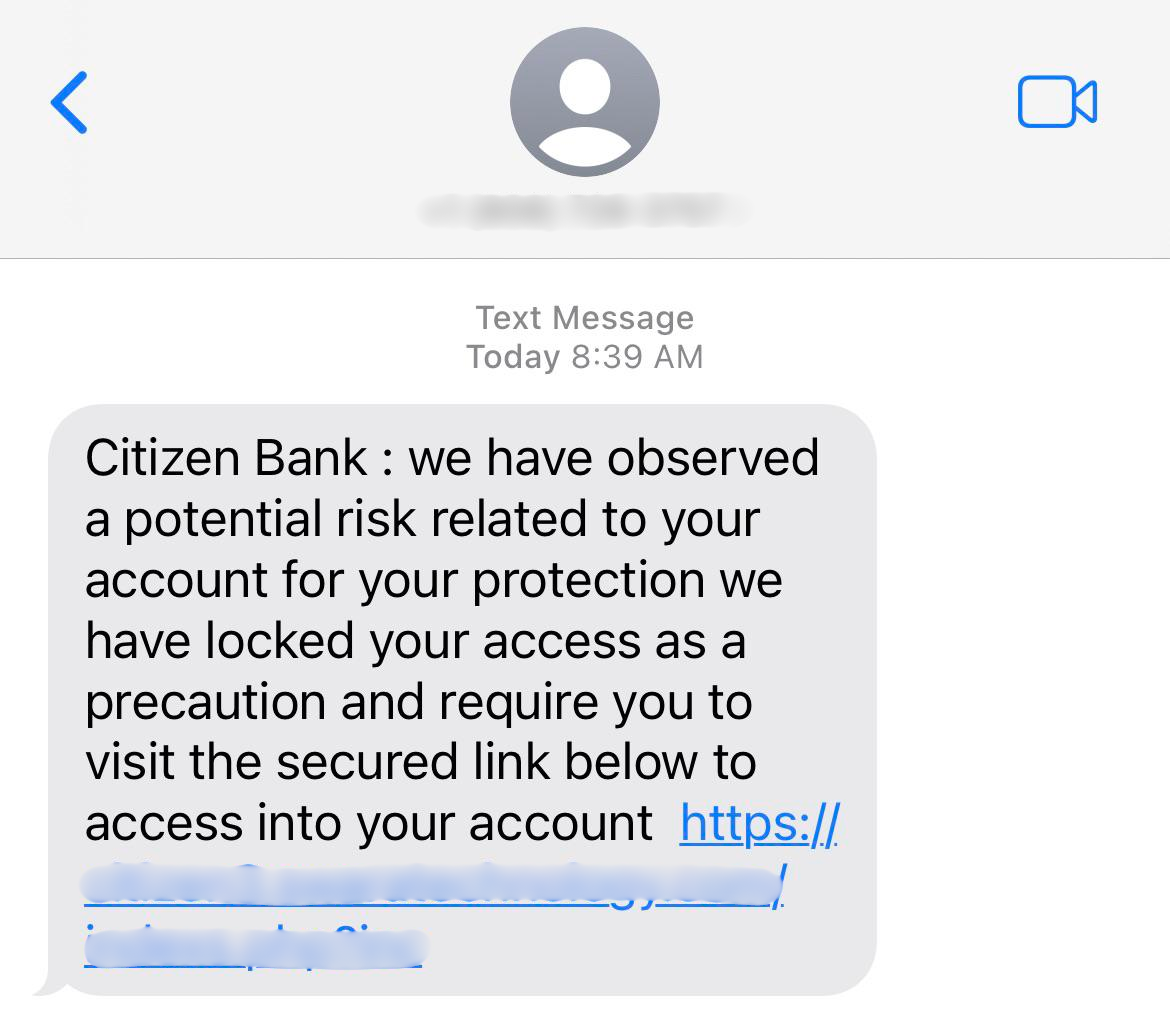

Example Scam Messages or Pop-Ups

The screenshot below is a real example of the type of communication used in bank impersonation scams. These messages are crafted to look and sound exactly like what your bank would send in a genuine fraud situation. Knowing what to look for helps you spot them before any damage is done.

Notice the urgent fraud alert language, the specific transaction reference designed to seem real, and the instruction to call back or click a link immediately. Real bank fraud alerts will typically ask you to confirm a yes or no on a specific transaction - they do not ask you to call a number from the text or verify your full account credentials. When in doubt, call the number on the back of your bank card directly.

Common phrases that appear in these scam messages include: we have detected unusual activity on your account and your card has been temporarily suspended, a transaction of $1,247 at an out-of-state merchant was flagged - did you authorize this, your account access has been restricted due to suspicious login attempts, please call our fraud hotline immediately to restore your account, and for your security we are moving your funds to a protected account. These phrases are chosen to create immediate concern and prompt action before careful thought.

Warning Signs

The following signals are strong indicators that a call or message claiming to be from your bank is fraudulent.

- You receive an unexpected call from someone claiming to be from your bank's fraud department. Even if the caller ID shows your bank's name or number, this can be faked.

- The caller asks for your full online banking password, PIN, or a one-time passcode that was sent to your phone. Your real bank will never ask for these over an inbound call.

- You are told to move your money to a different account to protect it from fraud. No legitimate bank will ever instruct you to do this.

- The caller asks you to send money to yourself through Zelle or another transfer service as part of reversing a fraudulent transaction. This is a common tactic to redirect funds to the scammer.

- The message creates intense urgency - your account will be drained, your card will be permanently closed, or legal action will follow unless you act in the next few minutes.

- A link in a text or email takes you to a page that does not match your bank's actual web address, even if the page looks exactly like your bank's real website.

- The caller tells you not to tell anyone about the call - including family members or other bank employees - because the investigation is confidential.

- You are asked to withdraw cash and hand it to a courier, deposit it into a Bitcoin ATM, or purchase gift cards as part of securing your account or resolving the fraud.

Who Scammers Often Target

Bank impersonation scams are sent broadly, but certain groups face a significantly higher risk of being drawn in by the approach.

Older adults are among the most frequently targeted. Many have substantial savings and are accustomed to taking calls from their bank seriously. The combination of a familiar brand name, a caller ID that appears legitimate, and an alarming claim about account security creates a scenario that is genuinely difficult to dismiss in the moment.

People who have recently experienced real fraud or had their card information compromised are also frequently targeted. Having been through a genuine fraud event makes a subsequent alert feel more plausible, and scammers sometimes obtain this information through data breaches and use it to add credibility to their approach.

Customers of large national banks - Chase, Bank of America, Wells Fargo, and others - are targeted most heavily, simply because the larger the customer base, the higher the probability that a mass-sent fake alert will reach an actual customer of that institution.

What the Scammer Is Trying to Achieve

The primary goal is access to your bank account. With your online banking credentials or enough account information to pass security verification, a scammer can drain your account, initiate transfers, or take over your account entirely by changing the contact information on file.

When the scam involves a safe account transfer or a Zelle payment, the goal is to convince you to move money yourself. This is particularly damaging because transfers you initiate are treated differently by banks than unauthorized transactions - they are often much harder to recover, since you technically authorized the movement of funds.

In some versions, the goal is simply information - account numbers, routing numbers, Social Security numbers, or enough personal data to open new accounts or take out loans in your name.

What To Do If You Encounter This Scam

If you receive an unexpected call, text, or email claiming to be from your bank about suspicious activity, the following steps will help you respond safely.

- Do not engage with the caller or respond to the message. If the contact is by phone, hang up. If it is a text or email, do not click any links or call any number provided in the message.

- Call your bank directly using the number on the back of your debit or credit card, or the number listed on your bank's official website. This is the only reliable way to verify whether there is a genuine issue with your account.

- Do not share your online banking password, PIN, or any one-time passcode with anyone who calls you, even if they appear to know your account details or sound completely professional.

- Do not transfer money to any account at the instruction of someone who called you, regardless of how the request is framed - including as protecting your money or reversing a fraud.

- Use a phone number lookup tool to check whether the number that contacted you has been flagged for scam activity before deciding on any next steps.

- Report the contact to the FTC at ReportFraud.ftc.gov and notify your bank directly so they can log the incident and alert other customers if needed.

How To Prevent Bank Impersonation Scams

Prevention comes from understanding how your real bank actually communicates and building habits that make these scams easy to recognize.

- Save your bank's official phone number in your contacts using the number on the back of your card or from your bank's website. Whenever you receive a call about your account, hang up and call that saved number directly instead of engaging with the inbound caller.

- Know that your bank will never ask for your full password, PIN, or one-time verification codes over an inbound phone call. If anyone asks for these, the call is not from your bank.

- Understand that no legitimate bank will ever ask you to move money to a different account to protect it from fraud. This is always a scam, regardless of how convincingly it is explained.

- Be cautious about caller ID. The phone number displayed on your screen can be faked to show your bank's official number. Caller ID alone is not proof that the call is from your bank.

- Set up account alerts through your bank's real app or website. Knowing what genuine fraud alerts from your bank look like - and how they arrive - makes fake ones much easier to spot.

- Talk about this scam with family members, especially older relatives. The single most protective habit is simple: hang up on any call claiming to be from the bank, then call the bank back directly using the number on your card.

- Consider using a phone number lookup tool when you receive an unexpected call from a number claiming to be your bank, to quickly check whether that number has been associated with scam activity.

Final Safety Advice

Bank impersonation scams are among the most convincing forms of fraud precisely because they mirror something your bank genuinely does. Fraud alerts are real. Banks do call customers. The process a scammer walks you through can feel exactly like the real thing, especially when the caller ID shows your bank's name and the caller sounds calm and professional.

The most protective habit is this: never act on an inbound call about your account. Hang up and call your bank back using the number on the back of your card. That one step breaks the scam entirely. Your real bank will understand. If there is a genuine issue with your account, it will still be there when you call back through the official number.

No real bank will ever ask you to move your money to protect it. No real bank will ever ask for your password or one-time passcode over the phone. Any call that does either of these things is a scam, regardless of how official it appears.

If you have been affected, contact your bank immediately, report what happened, and take steps to protect any accounts or personal information that may have been exposed. Acting quickly and working with your bank's fraud team gives you the best chance of minimizing the damage and recovering as fully as possible.